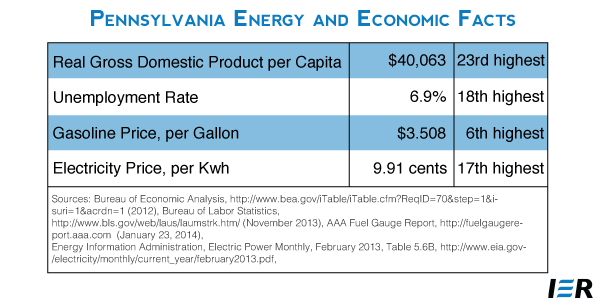

The Keystone State is experiencing record production for natural gas, largely due to a welcoming regulatory environment for hydraulic fracturing technologies that are unlocking vast reserves previously untouched in the Marcellus Shale. Meanwhile, the state’s coal industry has been suffering and the refining sector has felt the strain of federal regulations that are designed to cripple fossil energy producers. The Institute for Energy Research monitors closely the developments in this critical energy state, where unemployment and gasoline prices remain high compared to the rest of the country.

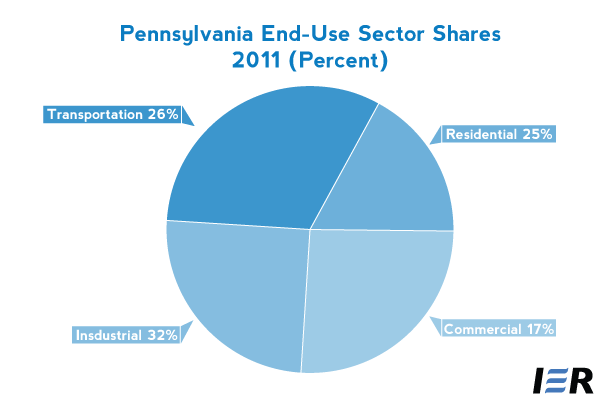

Pennsylvania is a leading supplier of coal, natural gas, nuclear power, and refined petroleum products to its own industries and the nation. Although it is among the top 10 consuming states for coal, natural gas, petroleum products, and electricity, its total energy consumption per capita is in the bottom half of states nationwide. The industrial sector leads consumption in the state with the following major energy-consuming industries: agriculture; mining; aluminum, steel and related heavy manufacturing; forest products; and tourism.

Source: Energy Information Administration, http://www.eia.gov/state/data.cfm?sid=PA

Pennsylvania’s State Rankings

- In 2011, Pennsylvania ranked 4th among the states in total energy production, producing 3,858 trillion Btu of energy.

- In October, 2013, Pennsylvania ranked 19th in oil production, producing 512 thousand barrels.

- In 2012, Pennsylvania ranked 3rd in natural gas production, producing 2,256,696 million cubic feet.

- In 2012, Pennsylvania ranked 4th in coal production, producing 54,719 thousand short tons.

- In October 2013, it ranked 5th in electricity production, producing 15,671 thousand megawatt hours of electricity.

- In 2012, Pennsylvania had the 15th highest average electricity retail price in the United States.

- In 2011, Pennsylvania ranked 32nd in total energy consumed per capita, consuming 292 million Btu per person.

- In 2010, Pennsylvania ranked 3rd in carbon dioxide emissions, emitting 256.6 million metric tons of carbon dioxide.

Fossil Fuels: Coal, Oil and Natural Gas

Pennsylvania is rich in fossil fuels, particularly coal and natural gas. In 2011, its energy production totaled 3,858 trillion Btu, the 4th largest in the nation, behind Texas, Wyoming, and Louisiana. The Appalachian Basin, which covers most of the State, holds substantial reserves of coal and more moderate reserves of conventional natural gas. The Basin’s Marcellus shale region contains reserves of unconventional shale gas.

Coal

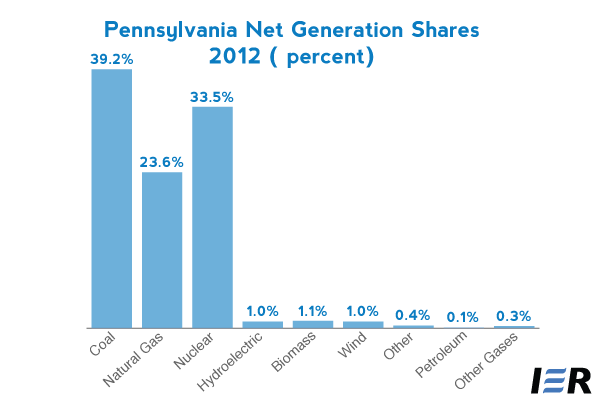

Pennsylvania was the fourth largest coal-producing state in the nation in 2012, and the only state producing anthracite coal, which has the highest heat value among the coal types. Northeastern Pennsylvania has the nation’s largest reserves of anthracite coal, a coal that burns cleanly with little soot, used primarily as a domestic fuel in either hand-fired stoves or automatic stoker furnaces. While Pennsylvania supplies virtually all of the nation’s anthracite coal, most of the state’s coal production consists of bituminous coal mined in the western part of the state, where several of the nation’s largest underground coal mines are located. Pennsylvania’s Enlow Fork Mine is the largest underground coal mine in the United States. In 2012, Pennsylvania produced 55.7 million short tons of coal—a fuel that dominates Pennsylvania’s power generation market, accounting for almost 40 percent of its net electricity production.

Pennsylvania is not only a major coal producing state; it is also a major coal consuming state. Most of its coal is used for electricity generation, but a small portion is consumed for steelmaking and other industrial uses.

Pennsylvania moves large quantities of coal by rail, barge, and truck, into and out of state. The majority of Pennsylvania-mined coal is used in the United States for electricity generation, about half in-state and half in other states throughout the east coast and the mid west. Pennsylvania coal consumers import nearly half of the coal they consume from nearby states. In recent years, a rising proportion of Pennsylvania coal has been exported to other nations. The state is among the nation’s leaders in coal exports.

Pennsylvania’s coal industry employed 52,000 people, with a payroll of $3.5 billion as of the summer of 2012. However, new regulations from the Environmental Protection Agency (EPA) are expected to put thousands of jobs in jeopardy and increase Pennsylvania’s energy costs. The new regulations due to the Obama Administration’s “war on coal” will result in coal-fired plant closings. Due to onerous regulations promulgated by the EPA, more than 3,000 megawatts of coal-fired power plants in Pennsylvania either have been prematurely retired or will be within the next 2 years. The majority of those retirements are announcements from the operators of the units; a few unit retirements are estimates from EPA models.

GenOn Energy Inc.,[1] for example, plans to close five of its older coal-fired plants over the next several years. The company indicated that new environmental regulations from the EPA will make it unprofitable to operate the plants, which have a combined capacity of 3,140 megawatts. The 5 plants are located in Portland, Shawville, Titus, New Castle, and Elrama, Pennsylvania.

PBS Coals Inc. and its affiliate company, RoxCoal Inc., laid off about 225 workers as part of an idling of some deep and surface mines in Somerset County, Pennsylvania in the summer of 2012, and now employ some 795 workers. “[T]he escalating costs and uncertainty generated by recently advanced EPA regulations and interpretations have created a challenging business climate for the entire coal industry,” said PBS Coals Inc. President and CEO D. Lynn Shank.

Natural Gas

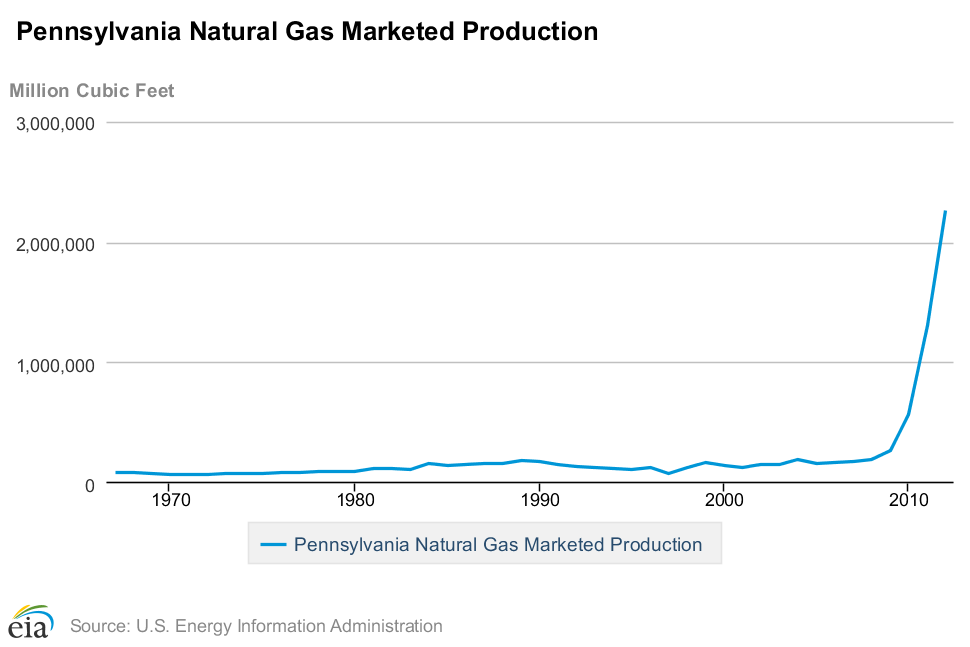

Between 2009 and 2012, Pennsylvania’s natural gas production increased by more than a factor of 8 due to expanded horizontal drilling combined with hydraulic fracturing in the Marcellus shale gas formation. The state now ranks third in natural gas production behind Texas and Louisiana. Estimates of proved reserves in Pennsylvania have also grown, increasing by a factor of 7 between 2009 and 2012. Hydraulic fracturing, which has been used for over 60 years with no confirmed case of groundwater contamination in one million applications, along with horizontal drilling has made Marcellus Shale extraction both economical and environmentally safe.

Source: Energy Information Administration, http://www.eia.gov/dnav/ng/hist/n9050pa2a.htm

Historically, natural gas exploration and development in Pennsylvania was relatively steady, with operators drilling a few thousand conventional wells annually. Prior to 2009, the wells produced about 400 to 500 million cubic feet per day of natural gas. With the increase in horizontal wells, Pennsylvania’s natural gas production increased by more than a factor of 8 since 2009, averaging nearly 6.2 billion cubic feet per day in 2012.

Pennsylvania’s electric power sector has grown rapidly in recent years to become the largest consumer of natural gas in the state, generating almost 24 percent of the state’s electricity in 2012. In terms of Pennsylvania’s natural gas consumption, the electric power sector is followed by the industrial sector, residential sector, and commercial sector in that order.

With the Marcellus Shale production, Pennsylvania meets its own natural gas demand and ships natural gas to other states via pipeline. Pennsylvania’s natural gas storage capacity is among the largest in the nation, which is being more heavily used with growing Marcellus production. New pipelines are being built to transport Marcellus gas to interstate natural gas pipelines. The state has some local pipeline infrastructure in the west from the days when western Pennsylvania, western New York, and West Virginia comprised the nation’s largest natural gas-producing region.

Oil

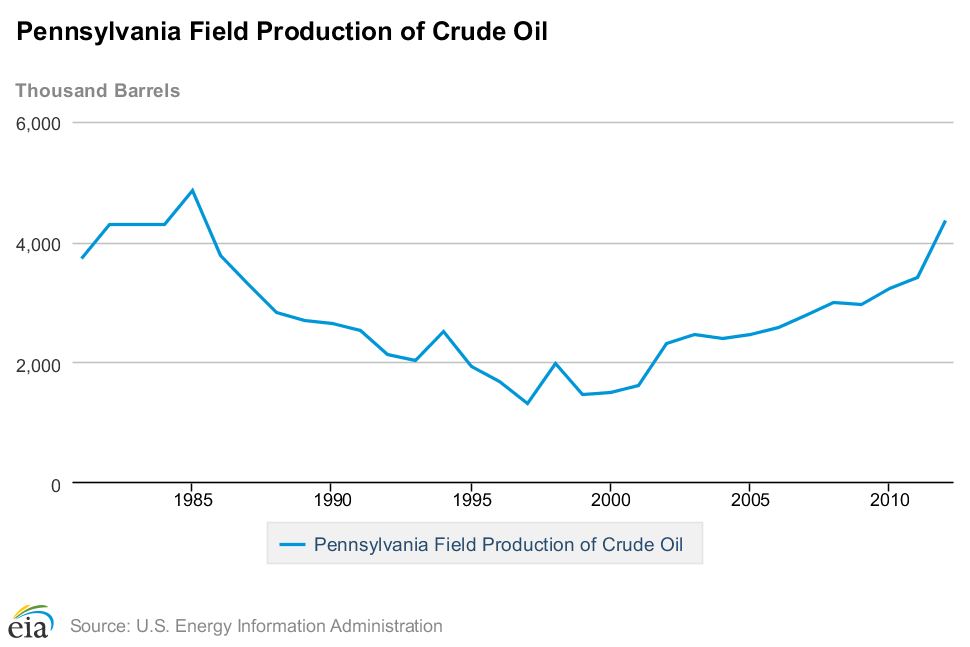

Although the first commercial oil well was drilled in Pennsylvania in 1859, the state’s current production of oil is small. In October 2013, Pennsylvania ranked 19th among the states in oil production. In 2012, the state produced 4,348 thousand barrels with much of the production coming from stripper wells.

Source: Energy Information Administration, http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MCRFPPA1&f=A

Pennsylvania has long been the leading petroleum-refining state in the Northeast. Until 2011, its three largest refineries, clustered on the Delaware River around Philadelphia, represented half the East Coast refining capacity. They supplied more than half the Northeast’s ultra-low-sulfur diesel and nearly half its heating oil and gasoline. Pipelines from these refineries transport products to other parts of Pennsylvania and to western part of New York State.

Because the refineries processed primarily imported crude oil, they struggled to compete as world oil prices increased. In 2012, new owners took over the two larger refineries and are improving their economics with less expensive feedstock from U.S. shale oil production, brought in mainly by rail. One refinery, at Marcus Hook, was converted to a refined products terminal.

In addition to petroleum products from local refineries, Pennsylvania receives refined products by the Colonial Pipeline from Texas and by tanker and rail from the Gulf of Mexico and Canada.

About one in five Pennsylvania households relies on distillate fuel oils for home heating, making Pennsylvania, like much of the U.S. Northeast, potentially vulnerable to distillate fuel oil shortages and price spikes. After severe weather threatened regional shortages in the winter of 2000, the federal government created the Northeast Home Heating Oil Reserve with three regional reserves in New England and the New York Harbor. In 2011, the government concluded that the harbor area had sufficient storage for the mid-Atlantic region and reduced the reserve from 2 million to 1 million barrels, all stored in New England.

The federal government also converted the reserve to ultra low sulfur diesel due to decisions by several Northeastern states to begin requiring ultra low sulfur diesel for heating. In 2012, Pennsylvania delayed its requirements because of uncertainty about operations at state refineries that were major sources of ultra low sulfur diesel.

Motorists in the heavily populated areas of southeastern Pennsylvania, including Philadelphia, are required to use reformulated motor gasoline blended with ethanol. Drivers in the Pittsburgh area must use a low-vapor-pressure motor gasoline blend in summer.

Electricity and Renewable Energy

Pennsylvania ranks fifth in electricity production in the nation and it exports electricity to adjoining states. Its electricity markets rely primarily on coal, nuclear and natural gas for electricity generation. While coal supplies almost 40 percent of its generation, natural gas-fired generation is a growing source, supplying almost 24 percent of net generation in 2012.

Pennsylvania’s five operating nuclear plants supply about one-third of the state’s electricity production. Pennsylvania ranks second in the nation after Illinois in nuclear generating capacity. Pennsylvania was home to the nation’s first commercial U.S. nuclear power plant in Shippingport, which came online in 1957 and was decommissioned in 1982 after 25 years of service. In 1979, a partial meltdown at Pennsylvania’s Three Mile Island nuclear plant resulted in the cancellation of new nuclear power plants in the country.

Pennsylvania generated about 3 percent of its electricity from renewable resources in 2012. The Susquehanna River and several smaller river basins provide hydroelectric power, and the Appalachian and Allegheny mountain ranges and the shoreline along Pennsylvania’s border with Lake Erie have wind power potential. Pennsylvania is among the largest users of municipal solid waste and landfill gas for electricity generation in the United States. Most of the state’s hydroelectric facilities have been modernized and upgraded for more efficient operation, having been in production for more than 50 years. Pennsylvania’s first commercial wind farms started operation in 2000. But, although installations are increasing, wind is still a small contributor to the state’s generation.

Source: Energy Information Administration, Electric Power Monthly, February 2013, http://www.eia.gov/electricity/monthly/current_year/february2013.pdf

Because Pennsylvania’s electricity production exceeds its in-state consumption, it supplies electricity to the Northeast. The regional electricity grid is operated by the PJM Interconnection, and the state’s wholesale power market is supplied with electricity almost entirely by independent power producers. With the increase in natural gas availability, the proportion of power generated from coal is declining, but coal remains the largest energy source for electricity generation.

Pennsylvania has an Alternative Energy Portfolio Standard that requires 18 percent of its electricity provided by generation and distribution companies to be produced from renewable sources by 2021. At least 0.5 percent must come from solar photovoltaic power. Pennsylvania is among the top 10 states nationally in grid-connected solar PV installations. Pennsylvania allows the following alternative forms of energy to meet its Alternative Energy Portfolio requirement: by-products of pulping and wood manufacturing, coal-mine methane, and waste coal.

Air Pollution Changes in Selected Cities

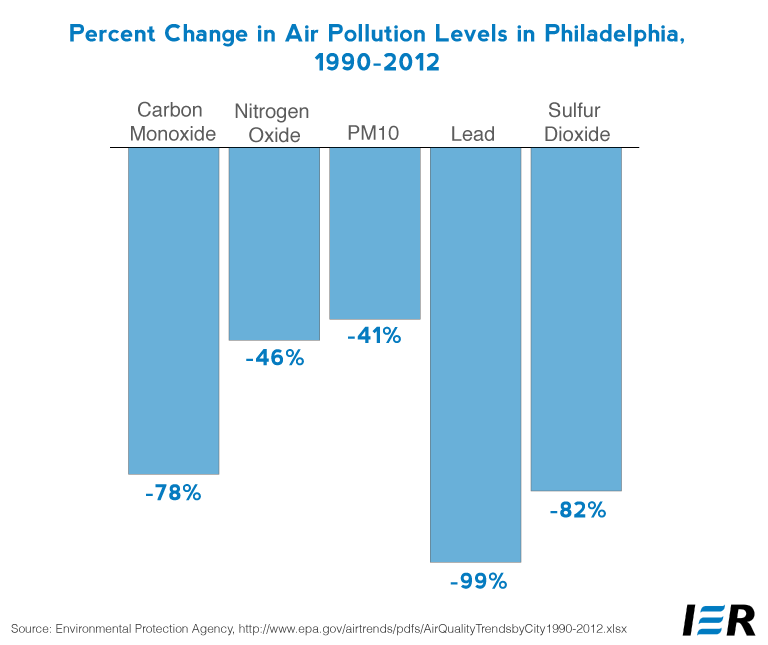

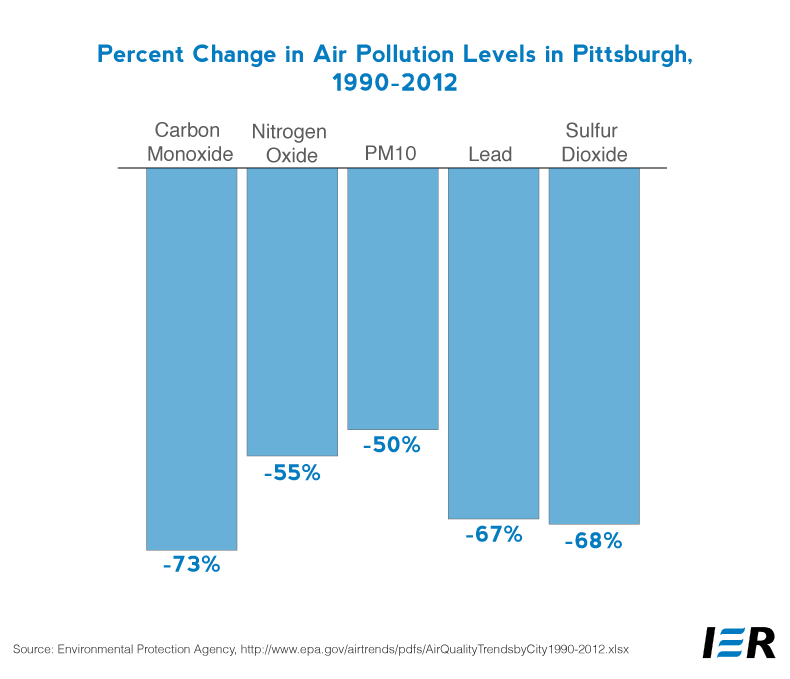

The Environmental Protection Agency (EPA) reports pollution levels for the criteria pollutants (carbon monoxide, nitrogen oxide, PM10, lead, sulfur dioxide) by city and state for the years 1990 and 2012. The following graphs show the reduction in these criteria pollutants over the 12-year period for Pittsburgh and Philadelphia. The reductions in Pittsburgh range between 50 and 73 percent, depending on the criteria pollutant and for Philadelphia , the reductions range between 41 percent and 99 percent, depending on the criteria pollutant.

Source: Environmental Protection Agency, http://www.epa.gov/airtrends/pdfs/AirQualityTrendsbyCity1990-2012.xlsx

Pennsylvania State Regulatory Environment

Below are some facts about Pennsylvania’s regulatory environment that are likely to affect the cost of energy or the cost of using energy. Although affordable energy is a vital component of a healthy economy, regulations frequently increase energy costs.

Pennsylvania is one of the 30 states that have a renewable portfolio standard (RPS) that mandates that a specified share of electricity be produced by renewable fuels in the future. Pennsylvania’s Alternative Energy Portfolio Standards require 18 percent of electricity sold by compliance year 2020 (June 1, 2020 to May 31, 2021) to come from renewable or approved alternative sources, including at least 0.5 percent solar photovoltaic power. The 18 percent includes 8 percent from Tier I resources (photovoltaic energy, solar-thermal energy, wind, low-impact hydro, geothermal, biomass, biologically-derived methane gas, coal-mine methane and fuel cells) and 10 percent from Tier II resources (waste coal, distributed generation systems, demand-side management, large-scale hydro, municipal solid waste, wood pulping and manufacturing products, and integrated gasification combined cycle coal technology). States that have an RPS tend to have higher electricity prices because renewable sources of energy are more expensive than their fossil fuel counterparts. Pennsylvania has the 17th highest electricity prices in the nation.

Pennsylvania also requires that utilities meet a portion of their electricity demand with energy efficiency. Act 129, adopted in October, 2008, requires utilities to implement programs to reduce consumer electricity demand. By May 31, 2013, in Phase I of the requirement, consumption must decrease by 3 percent from levels projected by the Commission for the June 2009 to May 2010 period, and peak demand must decrease by 4.5 percent from measured June 2007 to May 2008 peak demand levels.

The Pennsylvania Public utility Commission completed its first review of the program in August 2012, determining that the benefits of the program exceed its costs, initiating Phase II of the standard. Phase II runs from June 1, 2013 to May 31, 2016 and requires energy savings that vary by utility from 1.6 to 2.9 percent of electricity consumption measured between June 2009 and May 2010. Any savings above the 3 percent target of Phase I may be applied to the Phase II targets.

In Pennsylvania, investor-owned utilities must offer net metering to residential customers that generate electricity with systems up to 50 kilowatts in capacity; nonresidential customers with systems up to three megawatts (MW) in capacity; and customers with systems greater than 3 MW but no more than 5 MW who make their systems available to the grid during emergencies. Systems eligible for net metering include those that generate electricity using photovoltaics , solar-thermal energy, wind energy, hydropower, geothermal energy, biomass energy, fuel cells, combined heat and power , municipal solid waste, waste coal, coal-mine methane, other forms of distributed generation and certain demand-side management technologies.

Pennsylvania requires that all diesel fuel be mixed with at least two percent biodiesel one year after the in-state production volume of 40,000,000 gallons of biodiesel has been reached and sustained for three months on an annualized basis. Also, to reduce emissions of smog-forming pollutants, the state requires the motorists of the Philadelphia metropolitan areas to use reformulated motor gasoline blended with ethanol and the Pittsburgh area to also use specially formulated gasoline, 7.8 RVP, a fuel blended to reduce emissions that contribute to ozone formation.

Pennsylvania imposes automobile fuel economy standards similar to California’s to regulate greenhouse gas emissions from new vehicles. In 2006, the state’s Environmental Quality Board approved the Clean Vehicles Program to adopt certain of California’s vehicle emissions standards.

Pennsylvania requires new residential and commercial buildings to meet energy efficiency standards. Residential and commercial buildings statewide are required to meet the 2009 International Energy Conservation Code; and commercial buildings must also comply with ASHRAE 90.1-2007. These are codes that mandate certain energy efficiency standards.

Pennsylvania’s Executive order 2004-12 requires State agencies to purchase energy star appliances when economical and consistent with life-cycle costs.

Pennsylvania does not provide a cap on greenhouse gas emissions as do several states that are members of a regional agreement to limit greenhouse gas emissions. However, Pennsylvania is an observer of the Regional Greenhouse Gas Initiative, an agreement among ten Northeast states to limit greenhouse gas emissions, by 10 percent by 2018 through a cap and trade program. As an observer, Pennsylvania has no obligation to reduce its greenhouse gas emissions. Because there is no commercially available technology to control the release of carbon dioxide emissions, the most prevalent greenhouse gas emission, the cost of containment is particularly high resulting from either limiting the use of fossil fuels or increasing their prices. Carbon dioxide is a natural byproduct of the combustion of carbon-containing fuels, such as coal, natural gas, petroleum, wood, and other organic materials.

Conclusion

Pennsylvania is rich in energy resources, but threats from the federal government to further regulate the coal and refinery industries and to regulate hydraulic fracturing which has increased Pennsylvania’s natural gas production threaten the state’s economy and unemployment rate. Coal plants and mines are being closed in Pennsylvania because of the Obama Administration’s “war on coal.” Obama administration regulations and actions regarding fossil fuels are clearly negatively affecting employment and energy output in the state.

[1] NRG Energy acquired GenOn Energy Inc. in December 2012.