Key Takeaways

The EIA and Citibank forecast lower oil prices this year, resulting in lower gasoline prices.

EIA expects oil production from non-OPEC and OPEC+ producers to increase in 2025 and 2026 and outpace demand increases, resulting in lower oil prices.

Citi expects a larger oil supply surplus than EIA in 2025, resulting in a lower oil price forecast than EIA’s.

Significant uncertainties are embedded in both forecasts from the geopolitical situation in the Middle East and the Russia-Ukraine war with the associated sanctions.

The Energy Information Administration (EIA), in its January Short-Term Energy Outlook, is forecasting global oil prices (Brent crude oil) in 2025 to average $74 per barrel, falling to $66 per barrel in 2026. That is down from an average of $81 per barrel in 2024, or 8% lower in 2025 and 11% lower in 2026. The EIA forecast contrasts with Citibank’s lower price forecast for this year of $67 a barrel, which it raised from a previous forecast of $62 per barrel due to geopolitical risks centered on Russia and Iran. According to Reuters, Citi said the timing and nature of President Trump’s actions regarding Iran and Russia could be defining features of the oil market and pricing during 2025. The lower oil price forecasts result in lower expected gasoline prices, which EIA sees averaging $3.00 per gallon in 2026. Under Citi’s oil price forecast, that level will be reached sooner.

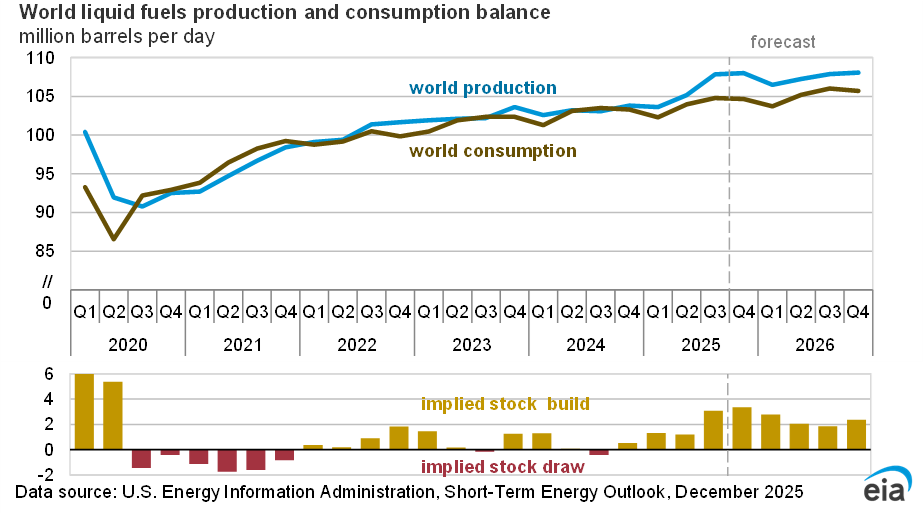

The lower expected oil price forecast is due to the expectation that global oil production will grow more than global oil demand. EIA expects strong growth in oil production outside of OPEC+ and an increase in oil production by OPEC+, but less than the group stated in its most recent production target to avoid significant inventory builds. This results in a significant surplus of oil production capacity in OPEC, as depicted in the graph below.

Growth in global oil production over the last two years has been led primarily by countries in North and South America, especially the United States, Canada, Guyana, and Brazil, which have increased their total liquid production by 1.1 million barrels per day in 2024. EIA expects that they will increase their production by an additional 1.0 million barrels per day in 2025 and 0.9 million barrels per day in 2026. EIA expects total global production of liquid fuels to increase by 1.8 million barrels per day in 2025 and 1.5 million barrels per day in 2026. Argentina is also a nation to watch, as its oil production is increasing rapidly under business-friendly President Javier Milei. They are soon expected to surpass Colombia in production in South America.

EIA expects global oil consumption growth to be less than the pre-pandemic trend. Global consumption of liquid fuels is expected to increase by 1.3 million barrels per day in 2025 and 1.1 million barrels per day in 2026, driven by consumption growth in non-OECD countries, particularly in Asia, where India is now expected to be the leading source of global oil demand growth. Citi’s lower oil price forecast in 2025 than EIA’s forecast is based on an oil supply surplus of 0.8 million barrels per day, larger than EIA’s expected surplus of 0.5 million barrels per day. China is reducing some of its demand for oil by mandating purchases of electric vehicles, for which they control global supply chains.

EIA expects U.S. oil production to increase to 13.5 million barrels per day in 2025, higher than the record in 2024 of 13.2 million barrels per day, and then average 13.6 million barrels per day in 2026 as oil operators slow production due to lower expected oil prices. Operators are expected to reduce the number of active drilling rigs as oil prices fall. EIA expects WTI prices to average $62 per barrel in 2026, down from $70 per barrel in 2025. The Permian region’s share of U.S. oil production is expected to continue to increase, accounting for more than 50% of all U.S. oil production in 2026. This increase is expected to be offset by contraction in other regions’ production.

Uncertainty Over OPEC+ Oil Production

OPEC+ producers agreed to their first round of reduced oil production targets and additional voluntary production cuts in April 2023 due to growing global oil inventories and falling oil prices that year. The latest agreement in December 2024 shifted the timeline for relaxing some of these cuts into 2026. Based on the expectation that oil production will continue to grow outside of OPEC+, it is uncertain whether OPEC+ members will continue adhering to lower production targets while countries outside of the group increase production and put downward pressure on oil prices. If the production cuts see diminishing returns relative to their impacts on oil prices and export revenue, the potential for dissent within OPEC+ could increase, leading some members to increase production unilaterally.

Geopolitical instability continues to pose a risk to oil production from various OPEC+ nations. Although oil shipments from the Middle East have not been directly impacted by conflict so far, ongoing tensions and recent unrest in Syria could escalate the threat to supply. Furthermore, upcoming policy actions by G7 countries, particularly concerning sanctions on OPEC+ members like Russia — such as the latest sanctions imposed — introduce additional unpredictability into the OPEC+ outlook.

Conclusion

The EIA and Citibank are both forecasting lower oil prices this year, resulting in lower gasoline prices. EIA expects oil production from non-OPEC and OPEC+ producers to increase in 2025 and 2026 and outpace demand increases, resulting in lower prices. Citi expects a larger supply glut than does EIA in 2025, resulting in a lower oil price forecast. There are significant uncertainties embedded in both forecasts from the geopolitical situation in the Middle East and the Russia-Ukraine war with the associated sanctions that could easily change the forecast, which is why EIA updates its short-term forecast monthly.