The Institute for Energy Research (IER) has formally submitted its Comment to the Office of Management and Budget on the Obama Administration’s use of the “social cost of carbon” as an input for federal regulatory action. This is a crucial topic that may significantly influence energy policy. Those who want the full details should click the link and read our full Comment, but in two posts here I am walking through the most important points we raised.

In our Comment, we objected to use of the “social cost of carbon” (SCC) in federal policy on several grounds. We grouped our objections into two categories, theoretical and procedural. In a previous post (“Part I”), I discussed the theoretical objections, meaning that even on purely academic or scientific grounds, it is very dubious to use SCC as a concept for guiding federal policymakers. In the present post (“Part II”), I’ll go through some of the major procedural problems, meaning that even if we thought the SCC made sense as an academic concept, the way in practice it is being used should show how dangerous it is in the hands of policymakers.

Ignoring OMB Guidelines

The Office of Management and Budget (OMB) offers clear guidelines on how federal regulatory cost/benefit analyses should be conducted, to ensure consistency and accuracy in the presentations for policymakers.[i] One of the guidelines is that all costs and benefits should be presented using both a 3% and a 7% discount rate. Another guideline is that the analysis should be conducted from a domestic perspective, rather than a global, meaning that the relevant figures are costs and benefits to Americans.

When calculating its estimates for the social cost of carbon, the Obama Administration’s Working Group ignored both guidelines. They reported their estimates from a global perspective, and the highest discount rate they used was 5%.

These omissions are striking, because in tandem they vastly inflate the official social cost of carbon. By the 2010 Working Group’s own admission, “a range of values from 7 to 23 percent should be used to adjust the global SCC to calculate domestic effects” (page 11). In other words, if we take the “official” SCC estimates that are being reported in the media and which are currently being used to analyze federal regulations, to comply with OMB guidelines these numbers should all be reduced by 77 to 93 percent.

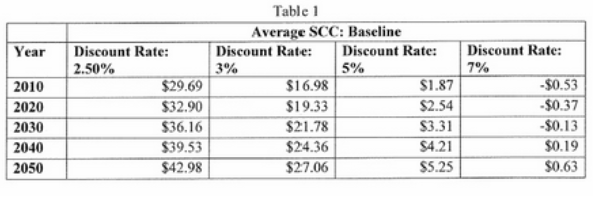

Yet that enormous adjustment merely concerns the domestic vs. global perspective. Ignoring the OMB guideline on discount rates is another huge matter. To see what a big deal this is, consider the Heritage Foundation’s analysis of the FUND model,[ii] one of the three used by the Working Group to generate its SCC estimates. The table below shows the FUND model’s estimates of the SCC at various discount rates, including the 7% rate that the OMB requires but that the Working Group for some reason ignored:

In light of the above results, it is no mystery why the Working Group chose to ignore these two crucial OMB guidelines. Had they heeded them—by reporting the SCC at a 7% discount rate, and using a domestic perspective—the estimated SCC would have been close to $0/ton for decades into the future. The entire rationale for the government’s crusade against carbon dioxide emissions would have collapsed. Rather than reporting the estimates under these parameters (as OMB required), and then having to explain why these numbers didn’t count, it was apparently less awkward just to ignore the OMB guidelines.

Cherry Picking Scientific Developments

Finally, it is troubling to note that the Working Group updated its estimates from 2010 to 2013 by heavily favoring those developments in the scientific literature that would increase the estimated SCC, while downplaying or ignoring those that would decrease it. This procedure results, of course, in an estimate of the SCC that is biased upward.

For example, as professional climate scientists Patrick Michaels and Paul Knappenberger explain in their own January 27, 2014 Comment submitted on behalf of the Cato Institute,[iii] the May 2013 TSD ignored the growing evidence in the peer-reviewed research that the “equilibrium climate sensitivity” parameter is lower than what had been used in the 2010 estimate. The equilibrium climate sensitivity (ECS) relates a doubling of atmospheric CO2 concentrations (relative to the preindustrial benchmark) to the long-term (including feedback effects) increase in average global temperature. The ECS is thus a critical input into the three computer models chosen by the Working Group to estimate the social cost of carbon. The higher the ECS, the more damaging a ton of carbon dioxide emissions will appear in these simulations, because it will cause a greater increase in global temperature and the assumed negative impacts following from this warming.

As Michaels and Knappenberger explain in their Comment, in the Working Group’s original 2010 report, there was a lengthy discussion about the probability density function (pdf) plugged into the computer models, which would reflect the discussion in the IPCC’s Fourth Assessment Report (published in 2007) on the distribution of possible values for the ECS.

Yet by the time the 2013 IPCC Report came out, there had been several papers calling into question the Fourth Assessment Report’s discussion. Indeed, the IPCC itself in 2013 admitted that it was lowering the bottom limit of the “likely” range of the equilibrium climate sensitivity from 2°C down to 1.5°C.

Even though the IPCC from 2007 to 2013 has reduced its (probabilistic) ranges of where the true ECS lies, the Working Group failed to revise the specific probability distribution function that it plugged into the three computer models. Had the Working Group revised the distribution downward, it naturally would have reduced estimates of the social cost of carbon across the board.

At the same time, the Working Group relied on several changes to their three chosen computer models that increased the SCC. To give one specific comparison, illustrating the rapid escalation of the estimate: The February 2010 Working Group report estimated the 2030 SCC, using a 3 percent discount rate, at $32.80. Yet just three years later, the May 2013 TSD estimated the 2030 SCC (again at 3 percent) at $52, a 59 percent increase.

Conclusion

In this post, we have gone over two major areas of procedural problems with the use of the social cost of carbon (SCC) for federal regulatory purposes. In publishing estimates of the SCC, the Working Group ignored two clear guidelines from the OMB, either of which would have drastically reduced the estimate. Further, when updating its numbers from the 2010 to 2013 report, the Working Group cherry-picked developments in the scientific literature, which helps explain why the estimate for the 2030 SCC (at 3% discount rate) increased a staggering 59 percent in just three years.

In light of the theoretical problems I outlined in the previous post, and the procedural problems I outlined in the present post, it is clear that the SCC is inappropriate for use in federal policymaking.

[i] OMB Circular A-4 available at: http://www.whitehouse.gov/omb/circulars_a004_a-4.

[ii] Dayaratna, Kevin and David Kreutzer. (2014) “Building on Quicksand: The Social Cost of Carbon.” Heritage Foundation, February 12, 2014, available at: http://blog.heritage.org/2014/02/12/building-quicksand-social-cost-carbon/.

[iii] Patrick Michaels and Paul Knappenberger, Comment for Cato Institute on “OMB’s Office of Management and Budget’s Request for Comments on the Technical Support Document entitled Technical Update of the Social Cost of Carbon for Regulatory Impact Analysis Under Executive Order 12866,” January 27, 2014, available at: http://object.cato.org/sites/cato.org/files/pubs/pdf/omb_scc_comments_michaels_knappenberger.pdf.